Shoppers browse in a supermarket while wearing masks to help slow the spread of coronavirus disease (COVID-19) in north St. Louis, Missouri, U.S. April 4, 2020. REUTERS/Lawrence Bryant/File Photo

WASHINGTON, Nov 15 (Reuters) - A year ago, as the coronavirus built toward its most intense peak, the U.S. economy was in a dark spot with job growth stalled, more than 10 million out of work and about to lose unemployment benefits, and warnings of a slide back into recession.

After the deployment of three vaccines and two rounds of government spending since, some measures of the economy have now hit pre-pandemic levels - and shifted the challenge for policymakers from battling a health crisis to determining which remaining problems are still rooted in the pandemic and which may need longer-term solutions.

Across issues as sensitive as racial employment gaps and as tangled as the path of inflation, that question will figure centrally in Federal Reserve and political debates over where economic and monetary policy should turn next, and whether those policies ultimately mesh or clash with each other.

The Fed's focus is on high inflation it hopes is mostly pandemic related and likely to ease without the need for higher interest rates. President Joe Biden's focus is on a just-passed $1 trillion infrastructure package and a follow-on $1.75 trillion bill focused on education, healthcare and climate change.

"We have been so focused on short-term recovery," said Nela Richardson, chief economist at payroll processor ADP, but "it is not just about going back to where we started, it is really taking stock of where we are and the structural changes that have been produced by COVID."

That could range from a workforce made permanently smaller by retirements, changes in work preference and declining immigration, to inflation shifted persistently higher because globally, she said, "the free flow of goods and services is not the same as it was."

IS THE RECOVERY COMPLETE?

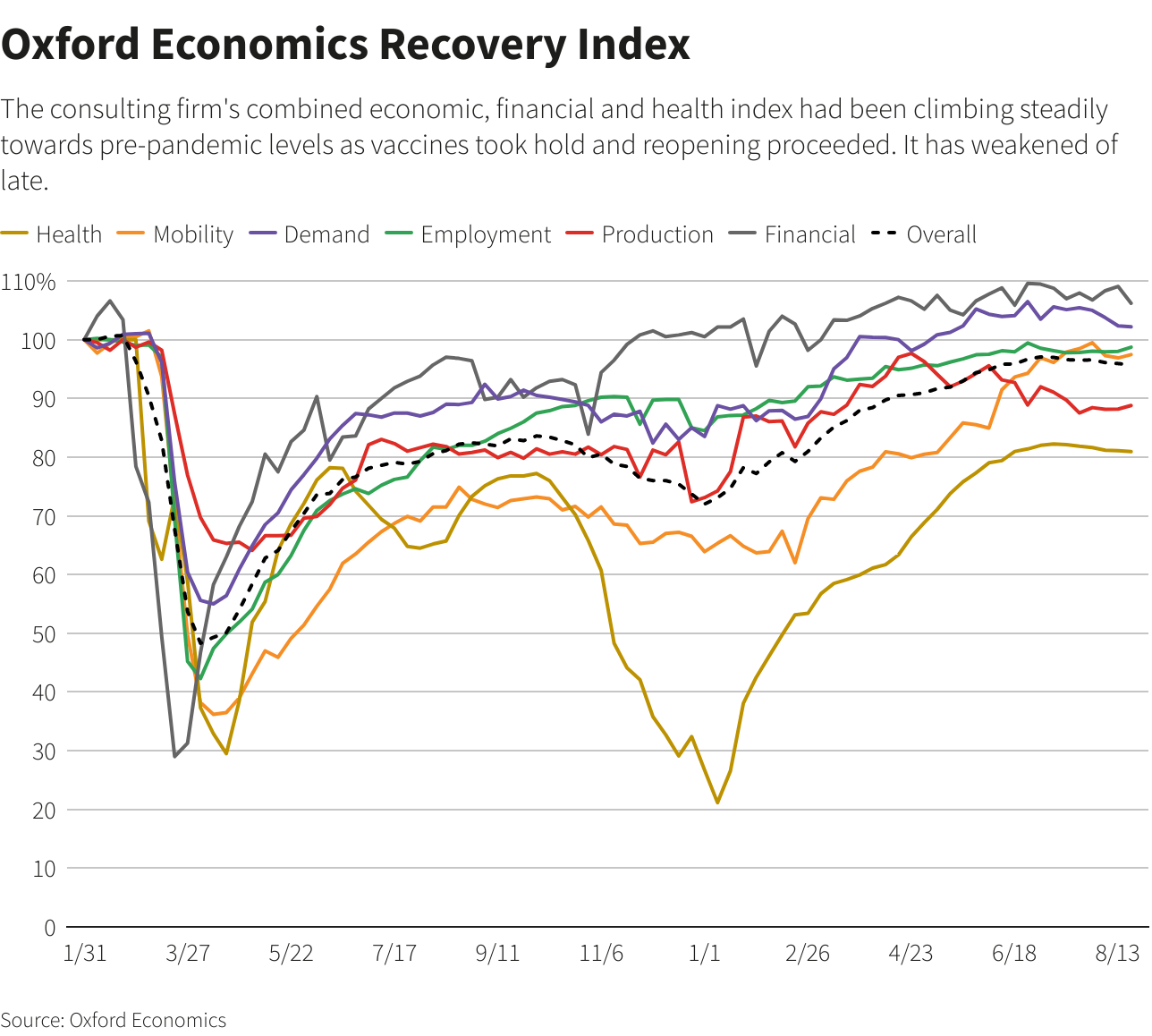

On Nov. 9, 2020, when Pfizer Inc (PFE.N) announced its COVID-19 vaccine was effective, an Oxford Economics "recovery tracker" stood at 80.5, nearly 20 percentage points below the start of the pandemic. It would go lower still, to 72, as the virus spread and firms unexpectedly shed jobs again.

Late last month it passed 100, meaning that across a combination of measures of production, employment, consumption and health, the economy was on net back where it started before the coronavirus.

That doesn't mean every metric had climbed to its starting point, just that for every remaining weak spot - hotel occupancy for example - something offsets it like a jump in restaurant visits or rising use of public transit.

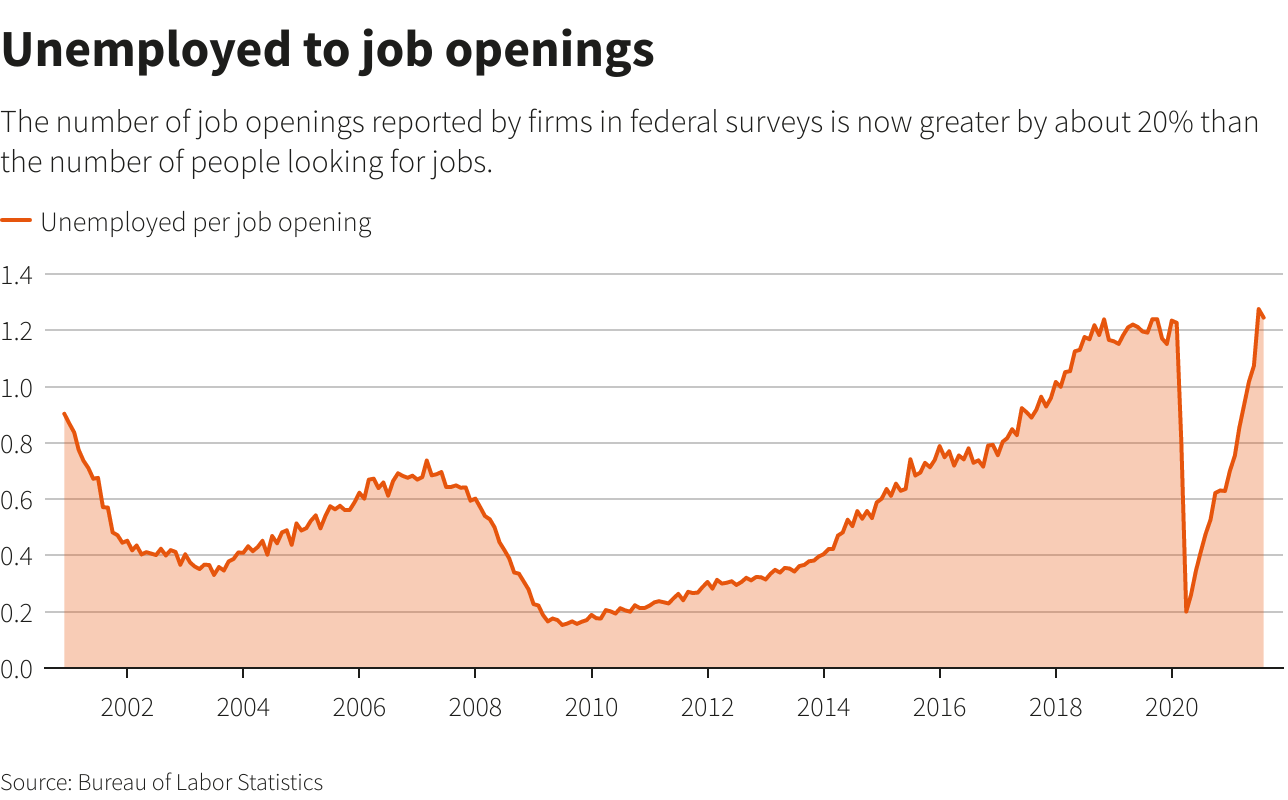

Similarly for the labor market, the remaining shortfalls are glaring. Some 4.2 million fewer people are on U.S. payrolls than in February 2020.

But the impulse seems there for continued job gains, between record numbers of job openings, rising wages, and people willing to quit jobs presumably for better ones. read more

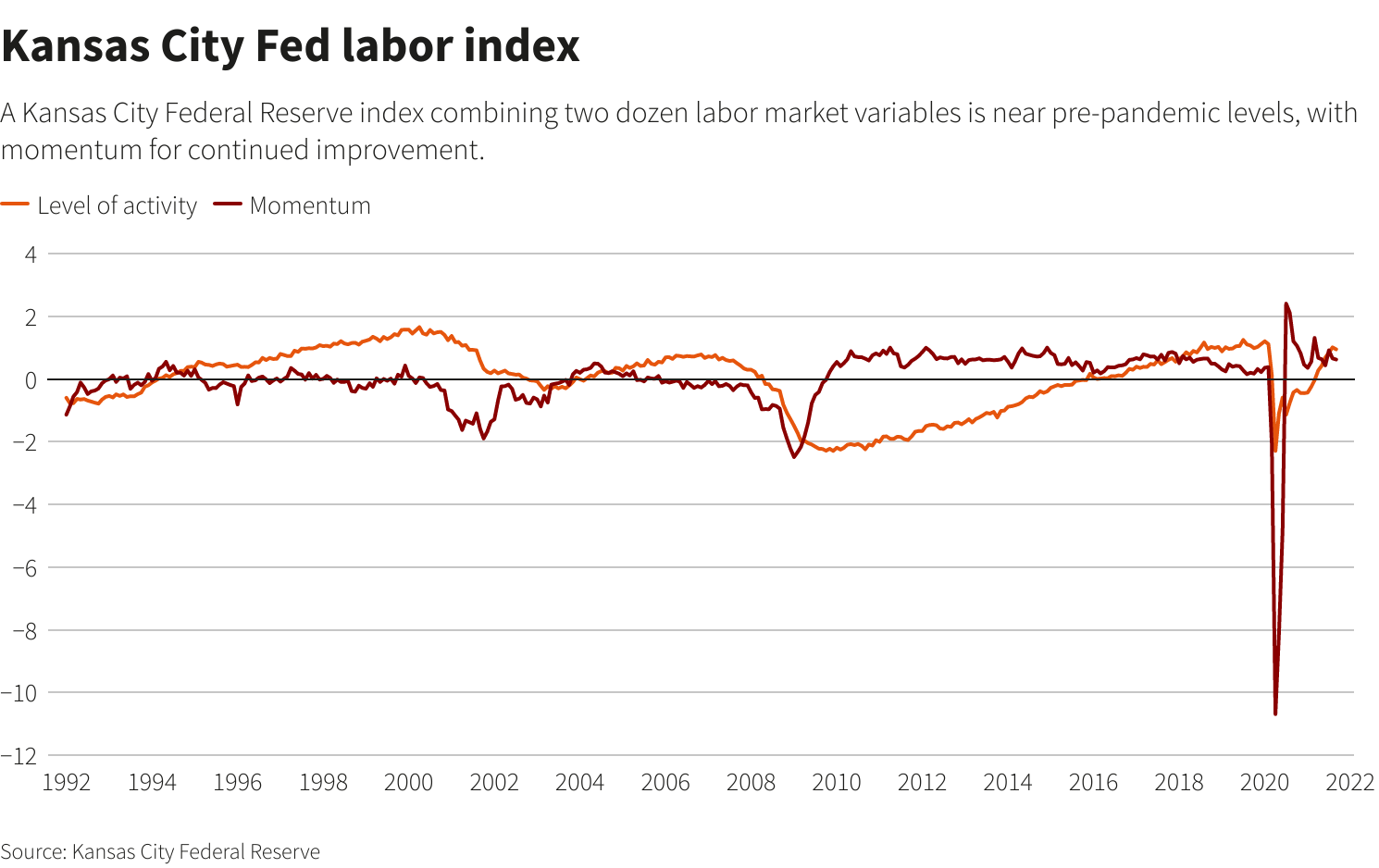

Many economists and Fed officials feel it is just a matter of time, perhaps another year, before the economy hits full employment. A Kansas City Fed labor market index shows a job market running well above its long-term average with still more upward momentum.

PANDEMIC FISSURES, OR SOMETHING MORE?

Outside the doors of the Kansas City Fed, that index would seem to match the facts on the ground. As of September, Missouri and neighboring Kansas had unemployment rates below 4% versus 4.6% nationally.

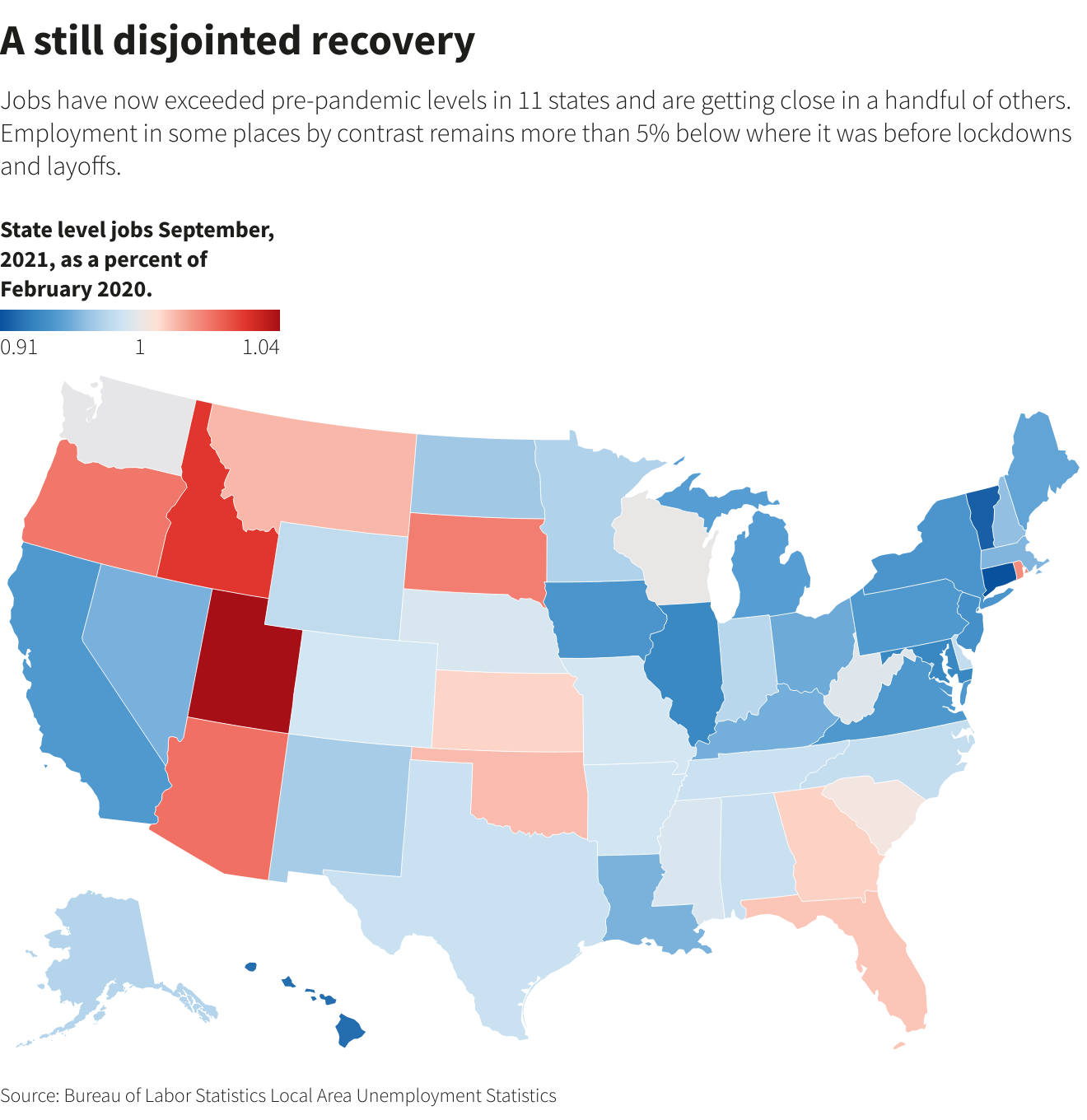

Bureau of Labor Statistics data shows employment in Kansas higher than in February 2020, with Missouri not far behind.

That's not true everywhere. In the industrial Midwest through the mid-Atlantic and New England employment is as much as 9% below the pre-pandemic level. The two largest state economies, California and New York, are both about 5% short.

The differences may stem from tradeoffs made earlier in the pandemic, with stricter health rules in some states suppressing the virus but tempering the recovery and looser restrictions in others allowing a faster jobs rebound at the cost of subsequent disease outbreaks.

But it poses a puzzle.

Are the lagging states still impacted by the pandemic and just need time to complete their bounceback? Or have their economies restructured around different industries or technologies that need fewer workers?

Similar questions surround the stalled labor force participation rate, still 1.7 percentage points below its pre-pandemic level, a gap of around 3 million people neither working nor looking for a job.

Research by Jefferies and others has estimated that, even at the lowest income levels, households have perhaps two months extra cash on hand from stimulus and other payments, including ongoing tax rebates for families with children, that may let them be more selective about work.

If people have left the workforce permanently, however, full employment may arrive sooner than anticipated. That has implications for the Fed, and for the Biden administration if the workers needed to staff new infrastructure or other programs become more difficult or costly to find.

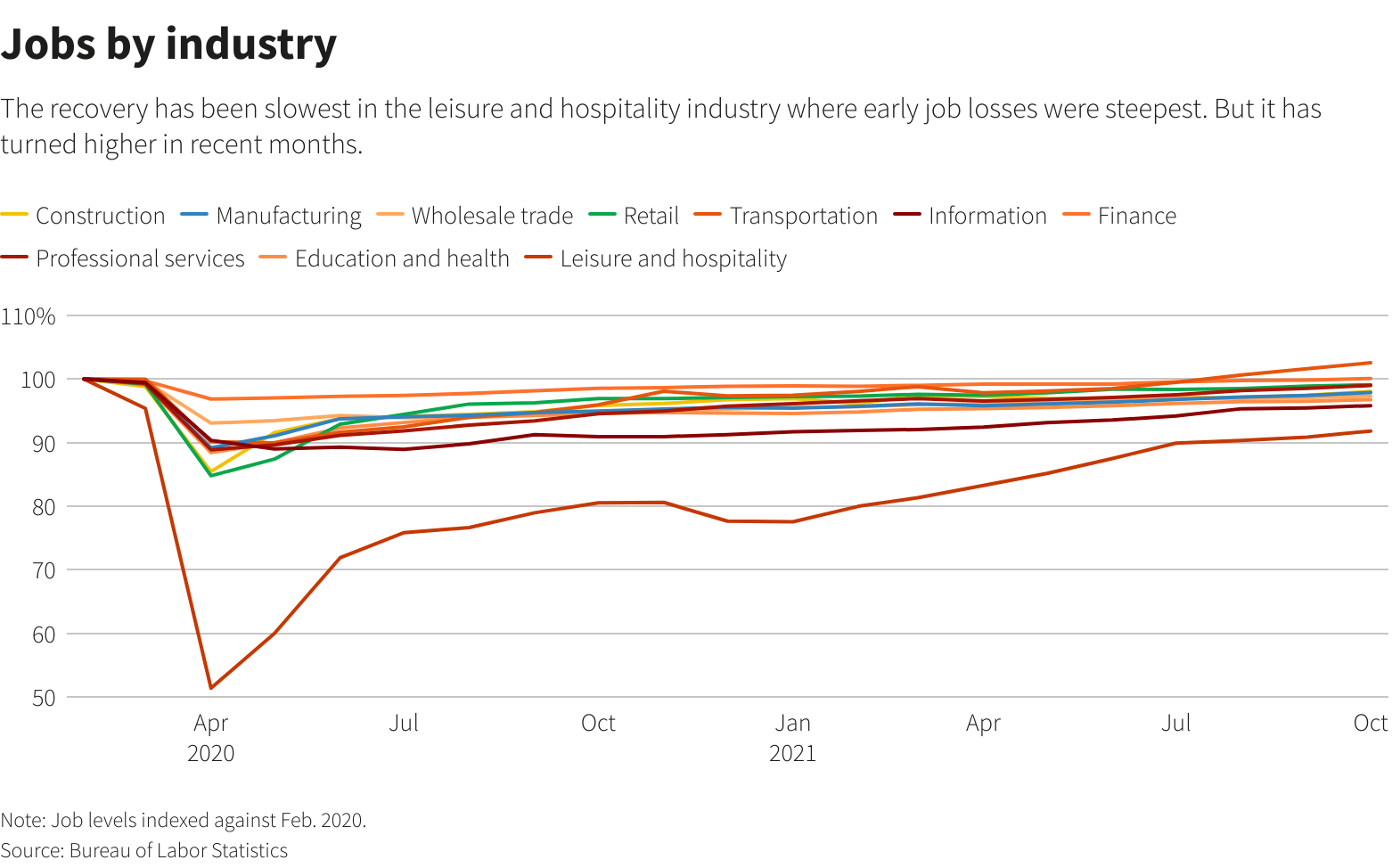

Job growth across industries has been uneven, too. Businesses that move goods now employ more people than before the pandemic, riding a surge in demand as the coronavirus shuttered sports stadiums, concert halls and other places where people ordinarily would have spent some of their money. Core service industries like leisure and hospitality are still nearly 10% short.

What's unknown is whether that evens out when spending shifts back to services, as many economists expect, or whether the occupational mix has changed for good.

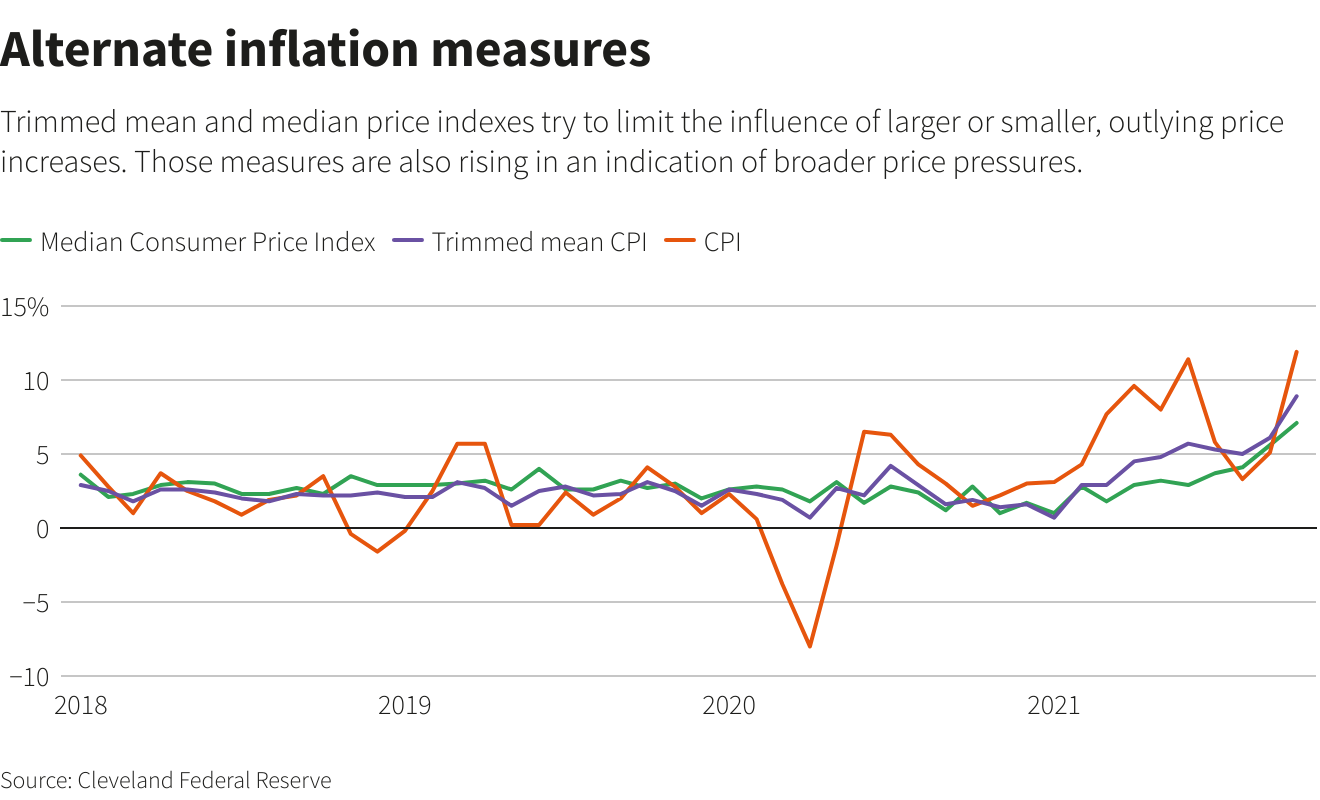

Likewise inflation may be running at a 30-year high because the recovery isn't finished, and will fall as spending, work and other habits return to normal.

But if something larger is in play - if a change in how inflation works has been mistaken for short-term supply chain or other pandemic disruptions - it could pose major risks.

"The risk is that (Fed officials) panic and chase down inflation" with faster and higher interest rate increases that could, Grant Thornton Chief Economist Diane Swonk wrote recently, "end our relationship with inflation but at a hefty price. It could tip the economy into a recession, or worse, if those hikes reverberate across developing economies."

Reporting by Howard Schneider; Editing by Dan Burns and Andrea Ricci

Our Standards: The Thomson Reuters Trust Principles.

"now" - Google News

November 15, 2021 at 06:07PM

https://ift.tt/3ciYEMc

Analysis: Post recovery? Fed, elected officials now challenged to define new normal - Reuters

"now" - Google News

https://ift.tt/35sfxPY

Bagikan Berita Ini

Related Posts :

Gameday Face Coverings Now on Sale at SHUPirateShop.com - SHU Pirates

Gameday Face Coverings Now on Sale at SHUPirateShop.com - SHU Pirates- Three Marines, Now Focus of Russian Bounties Investigation, Show the Costs of an Endless War - The New York Times

- Prepare for a winter covid-19 spike now, say medical experts - MIT Technology Review

- China has just contained the coronavirus. Now it's battling some of the worst floods in decades - CNN

- J.P. Morgan Chase now building reserves for a 'more protracted' downturn - MarketWatch

0 Response to "Analysis: Post recovery? Fed, elected officials now challenged to define new normal - Reuters"

Post a Comment